Learning to Live with Volatility (and profit from it)

(This piece first appeared in Founding Fuel Life)

March 2020 will be etched in market memory for a long time. The corona virus started off as a scare. In just a matter of weeks it had become a full-blown global contagion engulfing every nook and corner of global financial markets. In a single month the market had fallen 30% and individual stocks were down 40-70%.

This is how the market looked on 23rd March, 2020:

Imagine waking up and finding that a substantial part of your wealth had just evaporated.

With the benefit of hindsight, we now know that the pullback in the ensuing months was equally fierce. As of today, the overall market is up 100% from the 2020 lows and significantly higher than pre-Covid.

What a roller-coaster of a ride!

What is volatility?

Volatility is defined as a sudden change in prices. Typically, it is used to signify sudden fall in prices, because when market prices are volatile on the higher side, few people are complaining. Steep price declines invoke fear in the hearts of the most battle-hardened investors.

What causes volatility?

Investing is a continuous game, meaning that buyers and sellers are bidding prices of assets every day in the marketplace. This clearly implies that markets cannot keep going up in a straight line forever.

As a bull market progresses, there is increasing optimism and the prices of assets keep going up. New investors start joining in, and existing short-term investors start dominating the market. This is when stocks start moving 10%-50% in a day, and it becomes common knowledge that investments can double in a couple of months. It is a time of exuberance.

As time passes, every one who had to buy has already bought. There are no new buyers left. At this stage, any random adverse event can act as a trigger and lead to volatility.

The first leg of the volatility is viewed as a normal correction, and investors rush to buy stocks at lesser prices. But eventually stocks fall to such levels that the short-term holders are forced to resign and sell their positions. The market control moves back to the long-term investors.

Volatility ≠ Risk

Volatility is a temporary decline in stock prices, what is called quotational loss or paper loss. Though it may not feel so in the middle of a crisis, but volatility is not risk (for longer term investors).

Risk is defined as the possibility of losing permanent money on an investment. An investor takes on risk when investing in a company that is fundamentally not stable, or by investing in stocks at prices that they may never see again.

Volatility is not risk. And historic volatility does not necessarily project future volatility.

Volatility does not matter to long-term investors

Long term investors view volatility as a temporary dislocation in asset prices. It does not actually affect the long term prospects of businesses that they own. In the long term, the stock prices of businesses will reflect their business performance. Given this, long term investors hardly ever consider selling their positions in existing businesses.

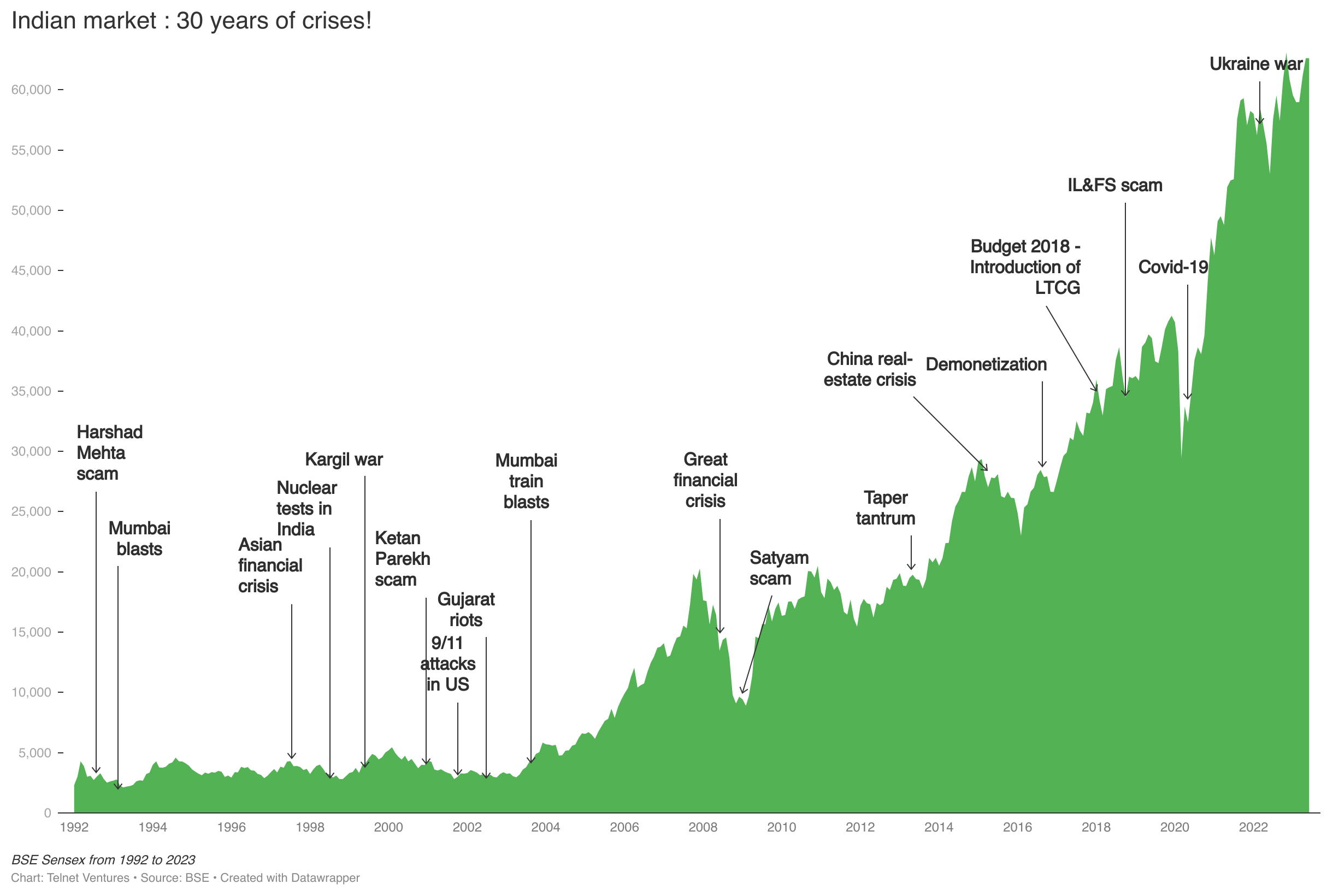

The chart below lists all the major crises of the last 30 years. Pick your favorite crisis. Demonetisation? Covid? Remember how dreadful it felt while it was happening? But look at what has happened to the markets subsequently.

While it is happening, volatility is gut wrenching for even the most experienced investor. The only difference is that experienced investors consider their fear as a signal that the current crisis is going to prove to be a great opportunity in hindsight.

No matter how calm you are, no matter how long term an investor you are, no matter what your horizons, when the market is jumping around, you feel uncertainty in your gut and it's hard to resist that.

If one anticipates volatility, why not sell and then buy cheaper?

It sounds like a smart idea to sell an asset while the prices are high and then buy it back at far lower prices. However, this is not feasible in actual experience.

Let us consider an investor who figures out that the market is at a top and sells all his holdings of a stock. As prices decline regularly, he is smug in the knowledge that he did the smart thing by selling out. However, the bottom is unknown in advance. After a significant fall, at some level the stock starts moving up. Typically, the first leg of this pull-back is as ferocious as the decline, and our investor is suddenly staring at prices far higher than what he saw just yesterday.

Psychology prevents the investor from buying at prices which are higher than yesterday, but significantly lower than the selling price at the top. A stock with long term potential has left the portfolio because of short term actions.

Bill Ackman, founder and CEO or Pershing Square, summarises this very eloquently.

We do not typically sell our core portfolio holdings even if we believe it is highly probable that they will decline in price in the short term, as long as our view of their long-term potential remains largely unchanged.

A short-term trading program might enable us to avoid a small loss at the much larger cost of missing substantial stock price increases thereafter. As a result, we do not trade around our long-term holdings...

If such smart global investors publicly admit of their inability to sell high and buy low, why must we smaller investors even entertain the thought?

Selling in the middle of volatility may be the worst thing to do

The drawdown in the portfolio during volatile market situations is just a paper loss. However, actually selling stocks during these situations creates real loss. See the table below and imagine that the investor had sold portfolio1 sometime in the first four years, just because he could not handle the price gyrations.

What a loss that would have been.

If you’re going to be in this game for the long pull....you better be able to handle a 50% decline without fussing too much about it.

Crises are the biggest chances to profit

Years of sharp declines are usually followed by equally sharp upside. Volatility creates a discount sale in the market which can be very profitable. Those who are new to the markets or sitting on cash can buy in such a flash sale.

But what is very interesting is how existing investors get the cash for buying in the next round of volatility. As the bull market progresses and frenzy gradually sets in, all that the long-term investors can do is periodically reduce their equity exposure (selling equity holdings and moving to cash), a process called re-balancing.

Note that, after every such sale, the market keeps moving up, making the investor look stupid at that time! However, in the bigger picture, the investor is creating the necessary war-chest to buy stocks at bargain prices when the next bout of volatility presents itself.

This is why looking foolish in bull markets is a necessary precondition for making money in the longer term.

It’s not easy to buy when the news is terrible, prices are collapsing and it’s impossible to have an idea where the bottom lies. But doing so should be the investor’s greatest aspiration.

Marks, co-founder of Oaktree Capital Management, wrote this memo in the midst of the Covid meltdown. Buying during crises can even be regarded as an intellectual pursuit!

Value-based investing - exploiting volatility

Most investors believe in investing in the latest trends and in companies that are talked about the most. However, there is another school of investors who focus on buying stocks of companies where they believe that the market price is substantially lower than the actual value of the company.

They believe that a good company bought at a steep price is an inferior investment to a bad company bought at a throwaway price.

The low price paid for a stock creates a margin of safety and ensures that the investor never loses his (substantial) capital.

For such investors, sudden bouts of market volatility, like during Covid, provide lucrative opportunities to swoop in and buy good companies at sale prices.

The true investor welcomes volatility.

It is my hope that the arguments and historical data convince you that volatility is a natural feature of the markets. Remember that the next crisis is always around the corner. It does not matter what it will be or how it will be eventually resolved. But what you can be sure is that, after it has passed, the price levels of most companies and the market indices will be higher.

{kind=link}

Member discussion