The Paradox of Liquidity

(This essay first appeared in Founding Fuel)

Liquidity in public markets allows for the seamless entry and exit of investments, offering flexibility but also encouraging detrimental short-term thinking. This liquidity fosters a focus on frequent trading and market swings instead of long-term business fundamentals. In contrast, private markets like venture capital and real estate, lacking real-time prices, promote thorough due diligence and long-term holding periods.

As we will explore, navigating this “liquidity paradox” requires a nuanced balance. While public markets allow for tactical positioning, their greatest advantage may lie in adopting the fundamentals-based mentality and long-term holding periods of private investors.

The Benefits of Liquid Markets

The appeal of liquid markets is clear: investments can be quickly entered or exited, serving key purposes such as:

- Non-Discretionary Needs: Quick access to cash for expenses like rent, taxes, and emergencies.

- Risk Management: Ability to adjust investments to manage risk.

- Opportunistic Investment: Capitalise on market opportunities with excess funds.

- Active Strategies: Enable strategies like momentum plays and sector rotations.

These benefits make liquidity indispensable for most investors. The Covid crisis highlighted this, as public market investors could sell assets for cash while private market investors were stuck with declining asset values. Real-time liquidity has become essential in modern investing.

The Pitfalls of Short-Termism

Constantly monitoring real-time prices drives investors to focus on short-term performance rather than long-term value. As Benjamin Graham noted:

“The development of the stock markets in recent decades has made the typical investor more dependent on the course of price quotations and less free than formerly to consider himself merely a business owner.”

This short-term focus undermines the skills needed for long-term wealth creation, such as business analysis, patience, and conviction. Many investors react to market declines without proper analysis, as Graham criticised, showing a lack of training in distinguishing price noise from fundamentals.

This leads to a culture of relentless trading and performance chasing, which undermines long-term investing principles. Excessive portfolio turnover often destroys wealth due to behavioural pitfalls such as:

- Overconfidence: Success in a few trades can lead to overconfidence and frequent, aggressive trading, often resulting in losses when the market turns.

- Disposition Effect: Selling winners too quickly while holding onto losers, often resulting in wealth destruction by missing out on long-term gains.

- Endowment & Loss Aversion: Investors irrationally value stocks they own and hesitate to sell losing positions, fearing to realise a loss.

These flaws stem from a focus on price movements over business fundamentals. Short-termism leads to “activity addiction,” where inaction feels uncomfortable.

This behaviour causes suboptimal portfolio turnover. Private equity funds hold companies for over a decade, whereas public market mutual funds turn over their portfolios every 1-2 years.

In his seminal 1949 work, The Intelligent Investor, Graham highlighted the dual-edged nature of public market liquidity:

“...what this liquidity really means is, first, that the investor has the benefit of the stock market’s daily and changing appraisal of his holdings, for whatever that appraisal may be worth, and, second, that the investor is able to increase or decrease his investment at the market’s daily figure — if he chooses. Thus the existence of a quoted market gives the investor certain options that he does not have if his security is unquoted. But it does not impose the current quotation on an investor who prefers to take his idea of value from some other source.”

A decade earlier, economist John Maynard Keynes was frustrated by investors’ “fetish of liquidity” and commented:

“The spectacle of modern investment markets has sometimes moved me towards the conclusion that to make the purchase of an investment permanent and indissoluble, like marriage, except by reason of death or other grave cause, might be a useful remedy for our contemporary evils.”

Both giants highlighted how the flexibility of liquidity cuts both ways — providing beneficial optionality, yet fostering a short-term trading mindset that hinders long-term wealth building

The Impatience Tax

Of course, private market investors aren’t compensated with premium returns over public markets purely due to illiquidity. The risks of investing in illiquid private equities — such as high failure rates, governance concerns, and pricing/valuation opaqueness — merit demanding a legitimate premium.

However, the psychological component of this “illiquidity premium” arguably represents a highly under-appreciated factor driving excess returns. By being forced into a paradigm of extensive upfront due diligence followed by near-permanent holding periods post-investment, private investors are saved from some of the self-inflicted wounds of public market investors who continually surrender long-term compounding for short-term trading.

This impatience premium is significant. Research shows private equity outperforms public markets by 7-8% annually, and venture capital funds demand an additional 3-8% premium.

Advantages for patient private investors include:

- Long Time Horizons: Investments held for 8-12+ years, ignoring short-term volatility.

- Deep Diligence: Thorough upfront analysis leads to high-conviction investments.

- Concentrated Bets: Focus on top opportunities rather than widespread diversification.

- Alignment: Fund managers invest their own capital, aligning their interests with investors.

- Control Position: Often securing controlling stakes for better operational oversight.

In effect, private investors are not only compensated for assuming illiquidity, but for methodically developing the psychological fortitude to resist short-term impulses that too often sabotage public equity returns.

Most times, holders of private assets remain blissfully unaware of the wild price fluctuations that could induce panic, precisely because there is no real-time ticker displaying each valuation gyration. Take the case of the global market rout during Covid-19. The same investors who watched listed stocks plummet 30-50% did not experience the same anxiety over their property or operating company holdings, as these lacked constant public price quotations.

This paradox did not escape the great Keynes, who astutely observed:

“(Investors) will buy without a tremor unquoted and unmarketable investments in real estate which, if they had a selling quotation available at each audit, would turn their hair grey. The fact that you do not know how much its ready money quotation fluctuates does not, as is commonly supposed, make an investment a safe one.”

One of my most illustrative experiences has been remaining an investor in a private foods company for over 10 years. As revenues compounded and marquee investors joined the capitalization table, there were no fluctuating stock tickers or “Sell” buttons constantly tempting me with the urge to cash out. Selling was simply not an option. I have no choice but to hold patiently through the entire growth cycle, whereas with a similar public company, impatience could easily have led me to leave staggering gains on the table prematurely.

Patience Pays Off

While liquidity offers flexibility, investors can incur substantial “impatience taxes” through excessive trading, as discussed. Paradoxically, those able to cultivate the fortitude of private investors may reap the greatest rewards in public markets.

Years ago, I backed a startup building enterprise software. While the founding team excelled, their unglamorous sector made venture capitalists wary, seemingly closing off any short-term exit for investors like myself. Had I been offered just a 2-3x return at that point, the temptation to cash out would have been intense. However, after (forcefully) persevering through nearly a decade, the startup was ultimately acquired by an industry titan at a staggering valuation — delivering supernormal returns to all parties involved. The lucrative outcome was made possible precisely because a lack of liquidity prevented an early exit.

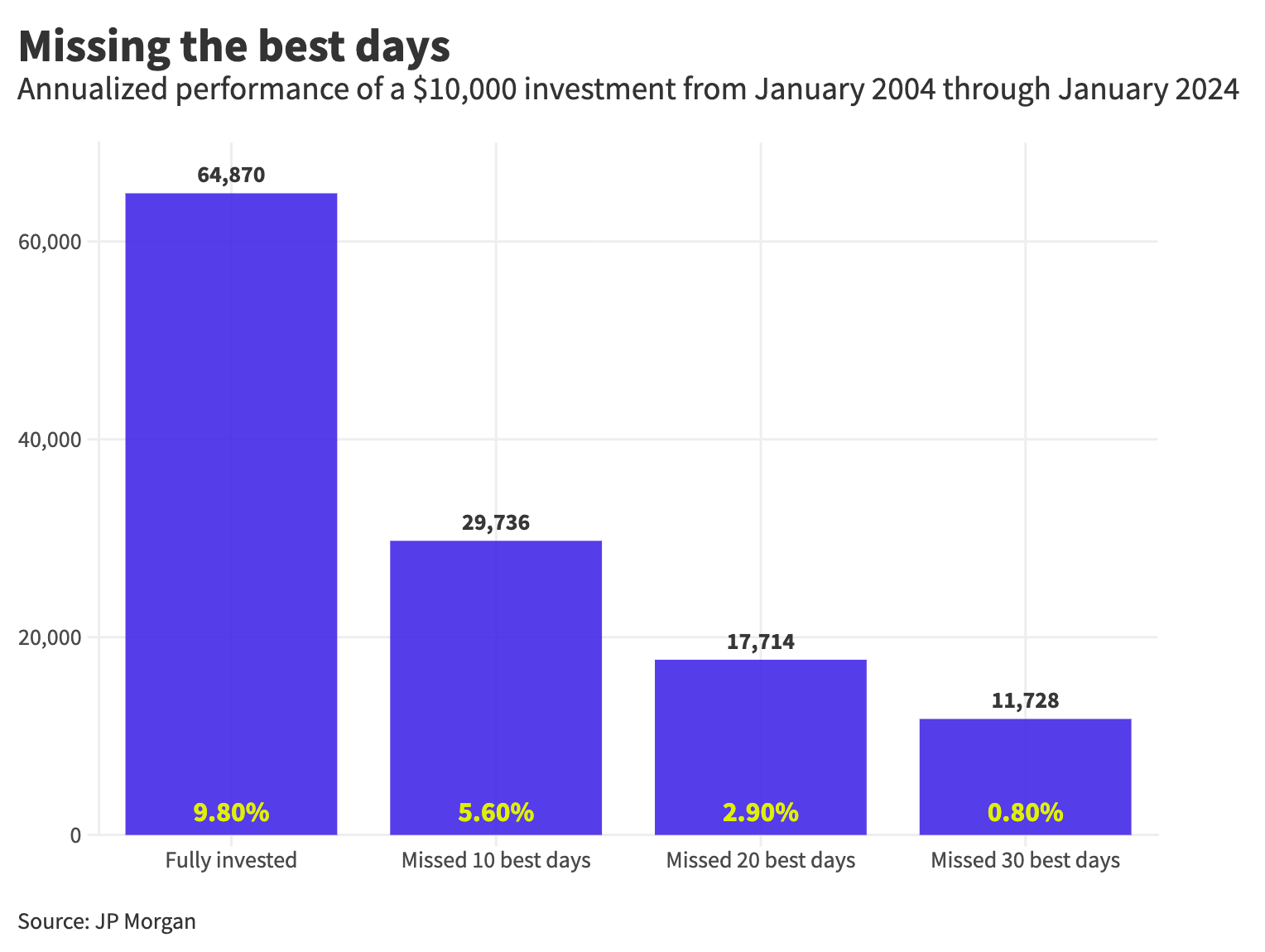

The compounding math in public markets is clear — missing just a few crucial days of returns can significantly hinder wealth creation over several decades, as the chart below depicts. This underscores the benefits of adopting a highly passive, “buy-and-hold no matter what” approach, concentrating solely on multi-year time horizons when strong conviction in fundamentals justifies such a strategy.

Graham astutely noted that when investors leverage liquidity to become short-term traders, they perversely transform their greatest investing advantage into a crippling disadvantage:

“The true investor scarcely ever is forced to sell his shares, and at all other times he is free to disregard the current price quotation...the investor who permits himself to be stampeded or unduly worried by unjustified market declines in his holdings is perversely transforming his basic advantage into a basic disadvantage. That man would be better off if his stocks had no market quotation at all, for he would then be spared the mental anguish caused him by other persons’ mistakes of judgement.” ##

Graham’s protégé Warren Buffett has similarly advocated the mental model of envisioning public markets closing down for a decade or more whenever establishing new core holdings.

Of course, this perspective represents an extreme paradigm shift from today’s video game trading mentality idolising quick, profitable entries and exits. Yet it emulates the exact patient approach of top private funds who repeatedly outperform public markets through systematically tuning out pricing noise over extensive holding periods.

For individual investors, developing a similar psychology may represent their greatest sustainable advantage in public investing.

The Ideal Liquidity-Patience Balance

While private patience carries its merit, public market liquidity remains invaluable in certain scenarios. Here are the key strategies to balance liquidity and patience effectively:

- Leveraging Liquidity for Initial Positions: Investors can prudently build initial investment positions through dollar-cost averaging, taking advantage of liquidity to spread purchases over time and reduce the impact of market volatility.

- Facilitating Intelligent Portfolio Rebalancing: Liquidity allows for intelligent portfolio rebalancing when asset allocations deviate significantly from targets due to market movements. Investors can:

- Trim concentrated positions that have appreciated.

- Add to positions that have become underweighted. - Taking Defensive Actions: Liquidity provides the flexibility to take defensive actions in response to evolving fundamental risks or unexpected thesis violations that materially impair an investment’s case. While patient investors avoid trading based on short-term market fluctuations, they may still use liquidity to reposition when high-conviction views demonstrably change.

- Conducting Extensive Upfront Due Diligence: Like private investors, public market participants should conduct extensive upfront due diligence to develop a shortlist of high-conviction ideas with superior long-term return potential.

- Establishing a Near-Permanent Mindset: These core holdings should be established with a near-permanent mindset, similar to private equity investors—maintaining the mental fortitude to ignore pricing noise and hold through complete business cycles lasting 5-10+ years, unless the original investment thesis becomes materially impaired.

- Bifurcate long-term and short-term portfolio: Even the smartest investor requires considerable willpower to maintain such extended holding periods across an entire portfolio. A more realistic approach is to bifurcate the total portfolio into:

- A Concentrated Core: High-conviction ideas sized for 5-10+ year horizons.

- An Actively-Traded Satellite Portfolio: A much smaller portion that trades more frequently.

By separating the ultra-patient core from a tactically-traded sleeve, investors can combine the private investor’s holding discipline with the judicious utilisation of public liquidity’s advantages—without the two working at cross-purposes.

Conclusion

Balancing liquidity and patience is crucial for sustainable wealth creation. Public market investors can benefit from adopting the long-term, fundamentals-based mindset typical of private investors. This approach allows them to enjoy the flexibility of liquidity while focusing on long-term value. By combining the best of both worlds, investors can navigate the markets more effectively and achieve their financial goals.

Member discussion